In any given year, Americans pass around roughly $89 billion in informal loans between friends and relatives, according to the Federal Reserve Board Survey of Consumer Finances as reported by Bankrate. A large share of that flows between people who share a last name. Lending money to family members is the master topic of this guide for adults: how the numbers actually move between siblings, parents and grown children, in-laws, and cousins, and why the simple math gets socially loaded the minute the cash lands. The page that follows is the map of nine recurring sub-topics. Use it to find your situation, read a worked dollar example, take one rule of thumb away today, and then click through to the deeper article that fits.

Key takeaways:

- Americans run about $89 billion a year in informal loans between friends and family, per the Federal Reserve Board Survey of Consumer Finances (via Bankrate, 2019).

- 42% of lenders never get repaid, and 49.9% never wrote anything down (Bankrate survey of more than 2,500 adults, 2019).

- The Internal Revenue Service (IRS) generally ignores intra-family loans of $10,000 or less; above that, the Applicable Federal Rate (AFR) sets a floor, with January 2026 short-term AFR at 3.63% per IRS Revenue Ruling 2026-2.

- Family caregivers spend an average of $7,242 a year out of pocket, or 26% of their income, on aging relatives (AARP Public Policy Institute, 2021 study of 2,400 caregivers).

- The ledger fixes the math; the conversation fixes the manners. Most family money fights happen when one is done without the other.

What family money among adults actually covers

Family money among adults is the set of cash flows that happen between grown relatives who no longer share a household budget. A 32-year-old fronting brunch for her sister and waiting to be repaid by Venmo. A 47-year-old splitting his mother's home-aide bill three ways with his two brothers. A 55-year-old lending her cousin $3,000 to bridge between a job loss and a new paycheck. None of these flows go through a bank loan officer. None of them involve a contract a court would enforce easily. All of them involve a ledger someone has to keep, even if that ledger lives in a head, a Notes app, or a group chat. Lending money to family members is the single most common form, and it is the head term of this whole topic.

The scope is wider than most people expect. A 2024 Pew Research Center study of young adults found that 44% had received financial help from their parents in the past year, and 33% had helped their parents financially. A separate Pew Charitable Trusts brief from 2016 reported that households facing material hardship were five times more likely than other households to have received money from friends or family. Family money is not a fringe topic. It is the second-largest pool of credit most Americans interact with after credit cards, and it follows none of the rules of the regulated kind.

This guide treats lending money to family members as one slice of a larger surface area. The other slices, paying back parents, splitting caregiving costs, dividing inheritances, settling who pays for the holidays, get their own pages later. Here you learn the lay of the land in a single read.

The math layer, where the numbers come from

The math layer of lending money to family members is the easy part. There are exactly four problems that show up over and over, and recognising which one you are facing is half the work.

The first is splitting. One person pays a bill, several people owe their share. Pizza on a Friday night. The cabin rental. The Mother's Day brunch. The cleaner who comes every two weeks to your father's apartment. Whoever fronted the money needs the others to settle up.

The second is lending. One person hands the other a sum and expects it back later. Three thousand dollars to bridge a job gap. Six hundred dollars to cover a security deposit. Fifteen hundred to keep a younger sibling's car on the road. There is a start date, a balance, and an implied or stated repayment window.

The third is settling. At the end of a group trip, everyone has paid for different things. Someone bought groceries, someone covered the rental, someone paid for gas. The group needs to compute who owes whom how much so the trip ends clean.

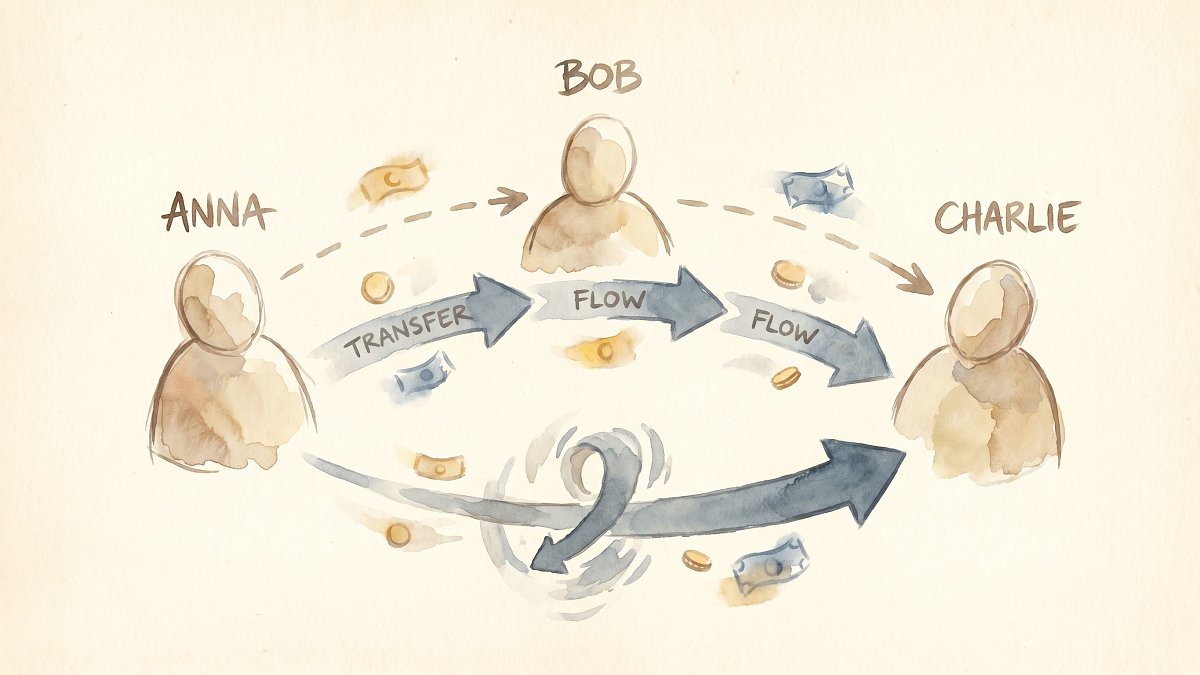

The fourth is simplifying. After a few months of an ongoing group like a sibling cluster covering a parent's expenses, the web of "Anna owes Ben $40, Ben owes Charlie $35, Charlie owes Anna $20" gets ugly. The canonical example from the Splitwise blog is Anna owes Bob $20 and Bob owes Charlie $20: rather than two transfers, Anna pays Charlie $20 directly and the chain collapses. Splitwise calls the feature Simplify Debts. Nudj calls the same mechanic Pass. The arithmetic is identical: net every member of the group to a single balance, then route the minimum number of payments to clear it.

All four problems are tractable arithmetic. Pencil and paper handle them; a spreadsheet handles them with less work; a ledger app handles them automatically.

A short worked example shows how fast a ledger gets ahead of a chat thread. Four siblings split a $4,200 weekend at a lake house. Sibling A pays the $2,100 rental upfront. Sibling B pays the $640 grocery run. Sibling C pays the $310 boat rental. Sibling D pays the $190 farewell dinner. Total spend $3,240; per-head fair share $810. The implied balances after the trip are A is owed $1,290 by the group, B is owed $170, C owes $500, D owes $620. A pen-and-paper ledger gets to the right answer in three minutes. Simplification lets the group close in two transfers (C sends $500 to A, D sends $620 to A, then A sends $170 to B) instead of four. The same logic generalises to every multi-party episode of lending money to family members across a year. The reason lending money to family members so often goes wrong is not the math; the math is solved.

The manners layer, where the awkwardness lives

The manners layer is where almost every fight about lending money to family members actually starts. Bankrate's 2019 survey of more than 2,500 adults found that 46.6% of people who had borrowed or lent inside a family or friend circle reported "serious arguments or conflicts" tied to the money, and 75.1% said they were no longer as close as they used to be. The dollar amounts in those breakups are often small. The damage is not.

What makes the manners layer hard is that it runs on unspoken rules nobody wrote down. Is this a gift or a loan? Will interest be charged or not? When does "I'll pay you back" become "you should have paid me back by now"? Whose business is it that one sibling has been quietly fronting more of the parent care than the other two? The math has answers. The manners only have answers if the family has had the conversation. Lending money to family members runs into trouble here, not in the arithmetic.

The Consumer Financial Protection Bureau (CFPB) offers a free worksheet titled "Managing family lending and borrowing" that turns the conversation into a checklist: is this a gift or a loan, how does it affect both parties in the short and long term, how does the relationship change if the answer is yes or no, what happens if it is not repaid. Nothing in that worksheet is complicated. The hard part is sitting down together and answering it. The rest of this guide assumes the math is solvable and focuses on giving you scripts, dollar examples, and named tools for the manners. Lending money to family members works only when both layers get attention in the same week.

Nine sub-topics inside lending money to family members

Family money among adults breaks into nine recurring contexts. Each has its own hub on Nudj. The short tour below is the master map; the linked hub pages go deeper on each.

Loans between adult siblings

Two adult siblings, one balance sheet for the loan, and the parents who may or may not know about it. The classic case is a 34-year-old lending a 31-year-old sibling $2,500 over six months to bridge between leases. The hub at loans between adult siblings, how it works without arguments walks through the math, the script, and the apps for this specific case of lending money to family members. Sub-pages cover the small favor loan without the awkward pause, the writing-it-down version of lending money to sibling, and the question of interest or zero, and how to keep it fair.

Caring for aging parents

The math here is heavier and the durations are longer. AARP's 2021 Caregiving Out-of-Pocket Costs Study, a survey of 2,400 caregivers, put the average annual out-of-pocket spending at $7,242, or roughly 26% of the caregiver's income. A 2025 AARP update reported 63 million family caregivers in the United States providing $600 billion in unpaid care a year. About 70% of people over 65 will need some form of long-term care in their lifetime. Within sibling clusters, the typical split debate is even shares, income-weighted shares, or hours-weighted shares for the sibling doing the hands-on work.

Inheritance discussions among siblings

Inheritance disputes between siblings often come down to a single word: equal versus equitable. The case for equal: simplicity, no judgment calls, no awkward defenses. The case for equitable: one sibling did 80% of the caregiving for the last four years, one sibling already received a $40,000 down-payment gift in 2014, one sibling has special needs that will outlast any estate. There is no universally right answer. The only wrong answer is leaving the question unsaid until the estate is in probate.

Borrowing from parents as an adult

Asking a parent for money at 35 is harder than asking at 21. The widely circulated National Debt Relief sample script puts the request in three parts: state the situation, list the steps already tried, propose a repayment plan with a number and a date. A worked version sounds like this: "Mom, I had a $1,400 car repair land on me this week, my emergency fund is down to $300 from last month's medical co-pay, and I am asking if you could lend me $1,100 to be repaid in four monthly installments of $275 starting in 30 days." Most parents say yes when they hear all three components, because the structure does the relationship work the request would otherwise force them to do alone. The hub on the mom-and-dad-finding-out fix, with a script covers the variant where a parent loan to one sibling becomes known to the others, which is a common follow-up problem in lending money to family members.

Paying back parents

Paying back parents is mostly about communication, not math. The CFPB worksheet covers the basic terms; the harder question is whether the parent secretly considers the loan a gift, whether the child secretly considers it interest-free for life, and whether either party will say so out loud. The repayment window, sorted in five minutes article walks through how to set a date both parties will remember.

Holiday gifts and family events

The math here is not the bill, it is the budget. Once a family has stepchildren, in-laws, and grown nieces, the holiday gift list scales nonlinearly. The widely cited "fair gift" rule of thumb is to set a per-relationship cap, agree on it before Halloween, and stick to it. Year-end events also reopen old lending balances: a December "let's just call it square" message is sometimes the kindest path forward.

Cousins, in-laws, and extended family

Lending money to family members gets thinnest at the edges. Cousins and in-laws live in the gray zone between "of course" and "I do not know you well enough to be your banker." The default norm in the United States is that adult cousins do not lend each other money in any significant amount, and in-laws lend only in directions blessed by the partner who is the blood relative. Both norms can be overridden by an explicit conversation, but the default is restraint.

Adult children living at home

The boomerang generation is now structural. A 2025 Empower and Thrivent survey found 46% of parents reporting an adult child aged 18 to 35 had moved back home. The dominant reasons are saving money (41%), inability to afford solo living (30%), and paying down debt (19%). Best practice: charge a token rent that funds an account in the adult child's name, write down a target move-out date, and revisit every six months. The article on working out lending money to sibling for uneven incomes translates directly to parent-child variants.

Helping family in financial trouble

When a relative is in real trouble (job loss, medical emergency, eviction), lending money to family members shifts from optional to urgent. The 2016 Pew Charitable Trusts brief found households in material hardship were 5x more likely than others to have received money from kin. The hub on what to do about covering a shortfall covers the typical structure, and a fair rule for what if they cant pay back covers the harder follow-up.

Two scenarios that happen every week

These are anonymized examples that recur across the Reddit r/personalfinance wiki on shared expenses, AARP caregiver community pages, and the Splitwise and NerdWallet help threads. Both are typical of lending money to family members in the 30-to-55 age band.

Scenario one: the small favor loan that stretched. Two adult siblings, both in their early thirties. Sister A asks Sister B for $400 to cover a vet bill on a Tuesday morning. Sister B Venmos the money in five minutes, no questions asked. Eight months later, Sister A still has not mentioned the money. Sister B does not bring it up because $400 is not worth a fight. The unresolved $400 quietly poisons two birthdays and one Thanksgiving. The fix is mechanical: a same-day Drop on a ledger app with a 90-day Nudge scheduled. According to the FinanceBuzz family lending survey, 54.5% of lenders end up asking more than once to be repaid, and loans documented in any form (text, email, app, paper) had materially higher repayment rates than oral-only loans.

Scenario two: three siblings, one aging parent. A 78-year-old father needs a paid aide twelve hours a week, total cost $1,860 per month. Three adult children, household incomes $58,000, $94,000, and $137,000. Equal-share math gives $620 each. Income-weighted math (proportional to combined income) gives roughly $389, $631, and $920 respectively. A third option, common in AARP-tracked families, gives the highest earner the cash bill and credits the local sibling for in-person time at a fixed hourly equivalent. None of these splits is automatically right. The right one is the one all three siblings agreed to, in writing, before the first invoice arrived. AARP's split-the-cost guidance walks through these models in detail.

Both scenarios share the same root cause: a five-minute decision at the start would have prevented a multi-year resentment. The whole point of a ledger like Nudj is to make that five-minute decision frictionless enough that families actually have it.

Who lends to whom inside a family

The shape of lending money to family members is asymmetric, and knowing the shape tells you who is likely to feel which kind of pressure. The 2023 FinanceBuzz survey on family lending found that parents (77.7%), siblings (75.8%), and grandparents (75.7%) were the three relations respondents were most likely to turn to for financial support. Cousins, in-laws, and adult children sat materially lower on the same list.

Flows by direction skew in the expected ways but with a twist. Pew Research Center's 2024 study of young adults found that 44% of 18-to-34-year-olds had received financial help from their parents in the past year, while 33% had also helped their parents in the same period; the two flows are not mutually exclusive, and lower-income young adults (43%) were almost twice as likely to help their parents financially as upper-income peers (19%). Parents in lower-income households were the most likely to receive help from their adult children (29% versus 9% for middle-income and 2% for upper-income parents). LendingTree's 2023 survey reported that 31% of Americans say a friend or family member currently owes them money. The picture is not one of stable, unidirectional generosity. It is closer to a busy network with most adults playing both roles in any given year.

The practical takeaway: when you set the manners for lending money to family members, expect the same relationship to run in both directions over a decade. The cousin you bridge in 2024 may bridge you in 2031. A ledger that captures both sides cleanly is worth more than a payment app that captures only the cash.

Eight common mistakes families make

This is the failure pattern we see most often in the surveys and community threads on lending money to family members. Treat the list as a methodology checklist, not as a sermon.

- Mixing gift money and loan money. The single biggest cause of family money fights, per a 2024 Charles Schwab guide. If the giver thinks "loan" and the receiver thinks "generous gift," both sides feel betrayed within a year. The fix is one explicit sentence at the moment of the transfer: "This is a loan, payback in twelve months" or "This is a gift, no strings."

- Skipping the written record. Bankrate's 2019 survey found 49.9% of family-and-friends loans were never put in writing, and 50.4% of lenders lost money on unpaid loans. The correlation is not subtle. Two lines in a chat thread count as writing if both parties are clearly part of the conversation.

- Ignoring the IRS tier for larger loans. The IRS only cares about written terms once a single intra-family loan exceeds $10,000. Above that threshold, the lender must charge at least the AFR (3.63% short-term, 3.81% mid-term, 4.63% long-term as of January 2026, per IRS Revenue Ruling 2026-2) or the foregone interest becomes imputed income to the lender and a deemed gift to the borrower. The federal gift tax annual exclusion sits at $18,000 per recipient for tax year 2024.

- Letting one sibling carry the caregiving load silently. Among the 63 million family caregivers AARP counted in 2025, the in-person caregiver is often also the one absorbing the highest out-of-pocket costs. Sibling clusters that explicitly equalize the load (whether by money or by hours) have measurably lower conflict rates in AARP's caregiver community surveys.

- Treating Venmo or PayPal as the ledger. Venmo and PayPal are payment rails, not ledgers. They record that money moved; they do not record that money is still owed. Lending money to family members works best when a separate ledger holds the "remaining balance" while a payment app handles the actual transfer.

- Lending what cannot be written off. The single AARP rule that turns up in every guide: if losing the money would change your life materially, do not lend it. Charles Schwab's 2024 guide adds a corollary: never lend money you would need within 18 months for your own retirement, mortgage, or medical buffer. Lending money to family members requires this discipline more than almost any other category of personal finance.

- Picking a tool before picking the layer. A bill-split app does not solve a manners problem; a long conversation does not solve a math problem. Skipping straight to the app is fast and feels productive, and leaves the manners conversation undone. The two layers need separate attention in the same week.

- Letting balances age past 90 days. The longer an unpaid balance sits, the harder both sides find it to mention. Most family money apps, Nudj included, default to a 30-day or 90-day reminder cadence for a reason: short cycles keep the relationship clean.

How four apps handle the core math

Most readers will already use, or have heard of, the apps in the comparison below for lending money to family members and friends. The differences matter only at the edges; for a family that simply needs a ledger, any of the four will do the basic math. The differences that show up over months of use are in friction, in nudge tone, and in whether the app feels like a tool for friends or a tool for accountants. For lending money to family members, all four apps fit the same basic mold.

| Feature | Splitwise | Tricount (bunq) | Settle Up | Nudj |

|---|---|---|---|---|

| Origin | US, independent, founded 2011 | Belgium/EU, acquired by bunq | Czech Republic, RealityShift | US, Nudj Labs |

| Free tier | Limited (daily add caps, ads) | Free, ad-free | Generous free | 100% free, no premium tier |

| Bank or card integration | None | bunq card prompts | None | None, by design |

| Debt simplification | Yes (Simplify Debts) | No | Yes | Yes (Pass) |

| Recurring groups | Yes | Limited | Yes | Yes (Tables) |

| Polite repayment reminder | Generic | Limited | Limited | Yes (Nudge) |

| Two-sided settlement | Manual | Manual | Manual | Yes (Square Up) |

| Money movement | No | No (bunq-only push) | No | No, ever |

All four apps are records, not banks. None of them processes payments. Nudj differs on two dimensions worth naming. First, it is permanently free with no ads and no premium tier, a non-trivial difference in a category where the leader Splitwise has progressively paywalled features on its free tier, as noted in BBC Worklife's 2022 feature on money among friends and the 2024 NYT Wirecutter roundup. Second, the named mechanics (Drop, Nudge, Square Up, Pass) mirror the social rituals that already exist between adult siblings rather than borrowing accountant vocabulary. Whether that matters to you is a matter of taste; the underlying math is the same in all four.

When to use a ledger app versus pen and paper or a chat thread

Three rules cover almost every case. Lending money to family members has a friction threshold, and the right tool depends on which side of that threshold the situation sits on.

Use a chat thread when the loan is below $50, the parties are in active communication, and the transfer will close within a week. The text history is the ledger, and dragging a chat into a separate app for a $20 cab fare reads as overformal. Most cousin-level lending sits in this band.

Use pen and paper, or a Notes app, when the loan is between $50 and a few hundred dollars, the relationship is close, and both parties are likely to forget which way the last few transfers ran. Pen and paper handles two parties cleanly. It does not handle five.

Use a ledger app when one or more of the following is true: the group is three people or more (siblings splitting a parent's care, roommates splitting a rent), the loan is recurring (weekly groceries, monthly subscriptions), or the relationship has any history of forgotten balances. The 2024 NYT Wirecutter roundup on bill-splitting apps and the NerdWallet roommates guide both reach the same conclusion: above three people or any recurring cadence, the marginal effort of using a real ledger pays for itself within a month. The threshold is not the dollar amount alone. It is the dollar amount times the number of relationships at risk. A $40 brunch among three siblings is a ledger event; a $400 loan between two close friends with a quick repayment cycle might not be.

Three rules of thumb worth memorizing

These three rules cover most of what a 30-to-55-year-old adult needs to remember about lending money to family members.

First, never lend what you cannot write off entirely. If you would feel genuine financial pain when the loan goes unpaid (and 42% do go unpaid, per Bankrate), the loan was too large or you were the wrong lender. Smaller and survivable beats larger and resented. AARP's 2022 guide on lending to loved ones makes the same point.

Second, always pair the math with the manners in the same week. Send the dollar amount on Monday, agree the repayment window by Friday, write both into the ledger by Sunday. Splitting the math and the manners across months is the single most reliable way to turn a $300 favor into a $300 grudge.

Third, let the ledger be neutral. When the awkwardness arrives, a ledger app's polite reminder ("Hey, just a heads-up: $400 still open from August") is easier on both sides than a human one. The whole point of a ledger like Nudj is to be the unflinching third party that neither sibling has to be when lending money to family members goes off-schedule.

FAQ: Lending money to family members

How much money do Americans lend to family in a year?

Total informal lending between friends and family in the United States runs about $89 billion per year, according to the Federal Reserve Board Survey of Consumer Finances cited by Bankrate. Within that pool, the average amount lenders have actually advanced is about $1,497, while borrowers have asked for $1,067 on average and currently owe $237 on the typical open balance, per the same survey.

Do I have to charge interest when I lend to a family member?

For loans of $10,000 or less, the IRS imputed-interest rules generally do not apply, so a zero-interest loan is fine. Above $10,000, the IRS expects the lender to charge at least the Applicable Federal Rate (AFR), which sits at 3.63% short-term, 3.81% mid-term, and 4.63% long-term as of January 2026 per IRS Revenue Ruling 2026-2. Below the AFR, the foregone interest becomes imputed income to the lender.

Is lending money to family members taxable?

The loan principal is not taxable; the borrower receives money and owes it back. Any interest paid is taxable income to the lender. If a lender forgives a loan, the forgiven amount may count as a gift and use part of the lender's annual federal gift tax exclusion, which sits at $18,000 per recipient for tax year 2024. The CFPB family lending worksheet walks through the tax checkpoints in plain language.

Should siblings split aging-parent care equally or by income?

Both work; the right answer is the one the family agrees to in writing before the bills start arriving. Equal shares are simplest. Income-weighted shares feel fairer when sibling incomes diverge widely. Hybrid models that combine cash from the higher earner with in-person hours from the geographically closer sibling show up often in AARP caregiver community pages. AARP's 2021 study put the average out-of-pocket cost at $7,242 a year per caregiver.

What if a family member never pays me back?

Forty-two percent of family loans go unpaid in full, per Bankrate's 2019 survey, so the scenario is common rather than exceptional. Three reasonable responses: convert the loan to a gift explicitly and in writing so the relationship has clean closure, accept a partial repayment plan with a longer window, or escalate to a formal promissory note if the amount and the relationship can support it. AARP's '5 Dos and Don'ts When Lending Money to Loved Ones' recommends never lending an amount whose loss you could not survive without bitterness.

Is Nudj a bank or a payment app?

No. Nudj is a social ledger. It records who owes whom and sends polite reminders when balances need attention. It does not process payments, hold money, or connect to bank accounts. Nudj is not a bank, money services business, or financial institution. Actual transfers happen through whatever rail the family already uses, such as Zelle, Venmo, a check, or cash, while Nudj keeps the ledger neutral.

How Nudj fits in

Nudj exists for the gap between the math and the manners in lending money to family members. The category leader Splitwise was founded in 2011 and has progressively paywalled its free tier; Tricount is bank-owned and trip-focused; Settle Up leans Android. Nudj is the social ledger built around the rituals that adult siblings, cousins, and grown kids already use with money: drop a debt, nudge a repayment, square up. Three product hooks matter most for family money among adults.

Drop and Nudge. Drop logs a balance in seconds. Nudge sends a polite reminder weeks or months later in language the sender chose, without the receiver feeling chased by a person. The Nudge handles the manners layer, not the math layer, which is exactly the gap most apps leave open when lending money to family members stretches past a few weeks.

Circles and Tables. Circles work for one-off groups (a wedding weekend, a family beach trip). Tables work for recurring contexts (a parent-care fund three siblings share, a roommates utility account, a monthly cousins' dinner). Tables are the structure most family money lives inside once you stop treating each transfer as a one-shot event.

Pass. Pass is the same debt-simplification mechanic Splitwise pioneered: it nets every member of the group to a single balance and routes the minimum number of payments to clear it. In sibling clusters where money flows in three directions over months, Pass cuts the number of payments by roughly half on average, which materially lowers the friction of lending money to family members in any recurring context.

Nudj is permanently free with no premium tier and no ads, available on the web today, with native iOS and Android apps shipping next. Nudj is not a bank, money services business, or financial institution; it never holds your money. Sign up at nudjlabs.com and start by inviting one sibling to a single Table. That five-minute step turns most of what this guide describes into ten seconds of friction the next time the cousin asks for $200 or the parent-care invoice arrives.

Conclusion

Family money among adults is larger, weirder, and more fragile than its dollar volume suggests. The Federal Reserve Survey of Consumer Finances counted $89 billion in informal flows a year between friends and family, and Bankrate's 2019 survey found 42% of those loans go unpaid and 49.9% never get written down. Underneath the volume, the failure mode is almost always the same: the math is solvable, the manners get skipped, and the relationship pays the cost.

The fix is small and durable. Pair every transfer with a one-line answer to "gift or loan?" Write it down within a week. Pick the right tool for the layer: a chat thread for the small, casual flows, pen and paper for the close two-person case, a ledger app for anything with three or more people or any recurring cadence. Lending money to family members works when the math is automatic and the manners are explicit, and almost any tool that respects both layers will outperform the silent version.

À lire également:

- Loans between adult siblings, how it works without arguments

- The small favor loan without the awkward pause

- The writing-it-down version of lending money to sibling

- Interest or zero, and lending money to sibling fairly

- Working out lending money to sibling for uneven incomes

- What to do about covering a shortfall

- The mom-and-dad-finding-out fix, with a script

- Repayment window, sorted in five minutes

- A fair rule for what if they cant pay back

Sources:

- Survey: Nearly half of Americans who lend cash to loved ones face negative consequences: Bankrate, 2019.

- Tips for managing family lending and borrowing: Consumer Financial Protection Bureau, 2024.

- Applicable Federal Rates: Internal Revenue Service, updated monthly.

- 2021 Caregiving Out-of-Pocket Costs Study: AARP Public Policy Institute, 2021.

- 5 Dos and Don'ts When Lending Money to Loved Ones: AARP, 2022.

- Debts Made Simple: Splitwise Blog, 2012.

- The best bill-splitting apps: NYT Wirecutter, 2024.

- How to split bills with your roommates: NerdWallet, 2024.

- Financial help and independence in young adulthood: Pew Research Center, 2024.

- How much money should you lend your friends?: BBC Worklife, 2022.

- How to Split Parents' Home Care Cost Among Siblings: AARP, 2023.

- Extended Family Support and Household Balance Sheets: Pew Charitable Trusts, 2016.